Could TikTok Coins be a threat to national security?

January 21, 2024 ☼ Payments

Discussions on TikTok and cryptocurrencies often address national security, but their intersection — TikTok Coins — remains less explored. TikTok Coins are digital currencies purchased with real money within the TikTok app. They are used to tip content creators during live streams and are categorized into values like diamonds and roses.

Unlike Meta’s failed Libra project, TikTok has taken a subtler approach. While Meta aimed to build a global payment system backed by reserves, TikTok restricts Coins to gifting creators and provides little public information about circulation or volume. Criticism has mostly been limited to isolated cases, like children overspending on Coins.

However, as TikTok’s creator economy grows, the platform’s rising revenue from Coins-based commissions could draw regulatory scrutiny. TikTok already faces questions about data collection from its billion-plus active users.

This leads us to the debate about whether TikTok should be banned. I lean towards free market principles and oppose arbitrarily banning businesses. After all, most concerns around TikTok center on the data it collects from its user base, which includes nearly 100 million Americans.

But other Chinese companies amass vast user data too. Take fast-fashion giant Shein. It arguably holds more sensitive information than TikTok (unlike TikTok, Shein knows your address). Should we therefore ban Shein too? Or ban all Chinese companies in the U.S. that reach a certain size? Banning TikTok could make the U.S. appear protectionist and anti-competitive, especially since users clearly find value in the app.

TikTok doesn’t pose a significant threat yet. Its largest current risks are user data and content algorithms. However, the stakes may rise if TikTok Coins grow in prominence. Collecting user financial data could elevate concerns beyond the realm of video preferences.

If TikTok Coins reach significant scale, the app must comply with payment regulations to prevent money laundering and illicit activities. Monitoring their growth is crucial, as they hold the potential to reshape online commerce.— NEXT FILE — Link: /debtcoin-governance Date: November 22nd, 2024 Tags: Crypto, Payments Comments: No

DebtCoin: Governance Framework

This article explores the governance architecture for DebtCoin, balancing centralized oversight with decentralized community input. Governance is divided into three categories: immutable components, upgradeable parameters, and hybrid processes. The goal is to ensure flexibility and stability while maintaining transparency as DebtCoin tracks the U.S. national debt.

Key Features of DebtCoin

- Pricing Mechanism: Value tied to U.S. national debt for inflation protection and transparency.

- Minting and Burning: Collateral changes as tokens are minted or burned.

- Reserve Management: Hybrid management of reserves in both DeFi (e.g., crypto) and TradFi (e.g., Treasury bonds).

- Debt Fluctuations: Mechanisms for rapid debt changes.

- Diversified Reserves: Adjusted composition to maintain stability and reduce risks.

- Dynamic Pricing: Recalibrated pricing via oracles.

Governance Components

1. Immutable Components

Core features hardcoded into the protocol:

- Price Calculation: Debt/10T formula.

- Minting/Burning Mechanics: Collateral-token relationship.

- Security Framework: Essential safeguards.

- Oracle Integration: Base for price feeds.

2. Upgradeable Protocol Parameters

Adjustable features via smart contracts, modified through on-chain voting:

- Reserve Ratios: Initial 100% USD backing, adjustable as needed.

- Transaction Limits: Caps on minting and burning.

- Fees: Dynamic fees (e.g., 1%) to fund operations.

- Oracle Settings: Data weighting and validation thresholds.

- Emergency Protocols: Circuit breakers (such as a 24-hour minting/burning pause) for extreme market shifts.

3. Hybrid Governance

Combines off-chain discussion and on-chain implementation. Examples:

- Reserve Composition: Community proposals for new assets like gold or crypto, executed through smart contracts.

- Liquidation Procedures: Debate off-chain, finalize on-chain.

4. Emergency Powers

Reserved for critical situations:

- Emergency Pause: Suspend operations during crises.

- Multisig Control: Consensus-driven operational decisions by the founding team.

- Strategic Oversight: Ensure alignment with the protocol’s long-term vision.

Decision-Making

Governance will involve both the community and founding team. Voting structures (direct, delegated, specialized tokens), and proposal rules and thresholds will ensure transparency and inclusivity.

Conclusion

This framework establishes a balanced governance model for DebtCoin, blending immutable rules, flexible parameters, and hybrid decision-making. Future articles will detail voting systems and community-driven proposals.

This is the third article in a 3-part series on DebtCoin:

DebtCoin: A Stablecoin Pegged to the United States National Debt

DebtCoin: Reserve Management

DebtCoin: Governance Framework (current) -– NEXT FILE — Link: /reserve-protocol-arbitrage Date: October 21st, 2024 Tags: Crypto, Payments Comments: No

Quick Notes on the Reserve Protocol — Arbitrage

“The RToken peg is maintained by allowing full minting and redeeming for the underlying collateral on-chain (Source)”.

But what if the arbitrage mechanism between the chain and secondary exchanges fails? Potential deviations can cause mistrust, leading to panic selling and potential system collapse.

I use this post to think about potential risks, arbitrage, and solutions to maintain trust and price stability. Arbitrage isn’t just a feature — it’s the first line of defense.

Risks to Arbitrage and Peg Maintenance

Illiquidity

If collateral can’t be liquidated during RToken redemption, panic selling may trigger a “bank run.” Exchange prices could collapse, and recovery depends on restoring liquidity and confidence.

Friction

High fees or slow processes make arbitrage unprofitable. Prolonged price gaps can arise, especially during network congestion

Protocol Design

Complex redemptions, high fees, or inefficient liquidation weaken arbitrage effectiveness during stress.

Regulatory Actions

Capital controls or trading restrictions may block on-chain or off-chain trading. If one major exchange fails, price stabilization depends on alternatives.

Extreme Volatility

High volatility deters arbitrage due to slippage or loss risks. Rapid swings can halt stabilization efforts.

Manipulation

Malicious actors could exploit friction to pump and dump, destabilizing markets and eroding trust.

Collateral Devaluation

Collateral devaluation or inaccessibility (e.g., During the SVB collapse, Circle lost access to some USDC reserves) can trigger panic and temporary depegging despite assurances of stability.

Mitigating Risks

1. On-Chain Liquidity

- Run stress tests to identify system limits.

- Monitor fees and set thresholds for dynamic pricing to prevent congestion from disrupting arbitrage.

- Establish clear processes to restore liquidity during crises (e.g., emergency minting or liquidity injections).

2. Off-Chain Activity

- Track RToken exchanges and liquidity to spot vulnerabilities.

- Assess security before listing on new platforms.

3. Technical Monitoring

- Identify early signs of smart contract vulnerabilities, protocol congestion, or governance issues.

- Automate alerts for unusual activity.

- Follow market sentiment on monitoring channels.

4. Regulatory Awareness

- Monitor regulatory shocks and diversify listings.

- Engage policymakers to understand emerging regulations.

5. Volatility Metrics

- Track exchange price deviations, redemption delays, and collateral liquidity.

- Use automated responses, like increased redemption incentives, to stabilize prices.

Conclusion

Arbitrage is key to maintaining the RToken peg, but risks like illiquidity, friction, regulation, and volatility can disrupt it. Mitigation through liquidity prioritization, monitoring, and proactive responses enhances stability and preserves the peg under stress.

This article is part of a series on the Reserve Protocol:

Notes on the Reserve Protocol — Governance

Notes on the Reserve Protocol — Arbitrage (current) -– NEXT FILE — Link: /reserve-protocol-governance Date: October 20th, 2024 Tags: Crypto, Payments Comments: No

Quick Notes on the Reserve Protocol — Governance

I’m planning to explore the Reserve Protocol, a fascinating cryptocurrency with a broad vision of improving lives and not just serving as a speculative asset. It aims to hedge against inflation, employs innovative technology and governance solutions, and supports citizens in struggling economies like Venezuela.

I’ll watch a series of videos by the founders and note my thoughts.

I’m starting with their governance videos.

Guardian Role:

The Guardian role’s veto power is designed to prevent governance capture. I wonder how it has been used in the past though. Transparency on past use and documentation of veto instances would build trust.

Who is the current guardian, and how are they chosen? Is it just founder Nevin? Could internal roles or a rotation improve oversight?

Community Engagement

Governance relies on RSR staking. Key questions:

- What proportion of RSR holders actively participate?

- How does it prevent minority capture or disproportionate voting power?

- Could engagement diminish over time, leading to disengaged decision-making?

Proposal Process

Proposals involve creation, voting, and time locks for security and safeguards.

- Are proposals executed on-chain or managed off-chain?

- What are the trade-offs between these methods in terms of security and accessibility?

Time Locks

How are urgent proposals handled?

- Do time locks cause delays in critical situations?

- Have delays or exploitation by bad actors occurred due to this mechanism?

Lessons from Compound

Reserve models its governance on Compound but avoids over-delegation issues that slowed decision-making. What specific lessons has Reserve applied?

I’ll continue watching their videos (they’re clear and accessible, the founders’ transparency builds trust). I’ll also join their communities, buy some RSR, and observe their governance mechanisms firsthand.

This article is part of a series on the Reserve Protocol:

Notes on the Reserve Protocol — Governance (current)

Notes on the Reserve Protocol — Arbitrage -– NEXT FILE — Link: /how-lego-stifles-innovation-limits-creativity Date: July 19th, 2024 Tags: Random Comments: No

How LEGO Stifles Innovation and Limits Creativity

LEGO’s design philosophy - starting with a destination and working backward - promotes a task-oriented mindset. Like puzzles, LEGO forces users into solving the narrow problems that it defines, a useful skill no doubt, but one that hardly stimulates creativity.

The focus on execution over exploration reduces the user to a cog in the assembly line, reminiscent of Adam Smith’s warnings about the division of labor creating soulless individuals.

Contrast this with an open-ended approach where each block sparks infinite possibilities. This is the mindset of an artist. Experimentation and creation become the journey and innovation emerges.

Adding to this are LEGO’s commercialization tactics. Their brand tie-ins and corporate partnerships turn users into products. The goal must not simply be to optimize, but create anew, a distintion that will only grow sharper as we enter the AI era where imagination and not efficiency will drive progress.— NEXT FILE — Link: /notes-terra-money-anchor-protocol-whitepapers Date: September 21st, 2024 Tags: Crypto, Payments Comments: No

Quick Notes on the Terra and Anchor Whitepapers

Exploring some stablecoin history today.

In this post, I jot down quick comments and immediate impressions while reading the Terra Money and Anchor Protocol whitepapers.

Terra Money

Instant Currency Swaps

A user can swap TerraKRW for TerraUSD instantly at the effective KRW/USD exchange rate. This allows all Terra currencies to share liquidity and macroeconomic fluctuations; a fall in demand by one currency can quicky be absorbed by the others.

Key flaw in the assumption that a fall in demand can quickly be absorbed by the others? This assumes the integrity of the overall Terra ecosystem and that there are no net outflows from the system.

Measuring Stability with Miner Oracles

Since the price of Terra currencies in secondary markets is exogenous to the blockchain, the system must rely on a decentralized price oracle to estimate the true exchange rate. We define the mechanism for the price oracle as the following: For any Terra sub-currency in the set of currencies 𝐶 =TerraKRW, TerraUSD, TerraSDR, .., miners submit a vote for what they believe to be the current exchange rate in the target fiat asset. Every 𝑛 blocks, the vote is tallied by taking the weighted medians as the true rates. Some amount of Terra is rewarded to those who voted within 1 standard deviation of the elected median. Those who voted outside may be punished via slashing of their stakes. The ratio of those that are punished and rewarded may be calibrated by the system every vote to ensure that a sufficiently large portion of the miners vote.

Issues to consider:

- Median price may not always reflect true price

- If Terra loses its value, voters may be disincentivized to align with the true/median price

- Risk of voters colluding to coordinate on a false price

Achieving Stability with Consistent Mining Rewards

Once the system has detected that the price of a Terra currency has deviated from its peg, it must apply pressures to normalize the price. Like any other market, the Terra money market follows the simple rules of supply and demand for a pegged currency. That is: Contracting money supply, all conditions held equal, will result in higher relative currency price levels. That is, when price levels are falling below the target, reducing money supply sufficiently will return price levels to normalcy. Expanding money supply, all conditions held equal, will result in lower relative currency price levels. That is, when price levels are rising above the target, increasing money supply sufficiently will return price levels to normalcy.

Flaws:

- “All conditions held equal”

- Contracting/expanding money supply requires (1) leveraging reserves (2) minting. 1 has its limits, 2 doesn’t necessarily stabilize price if buyers aren’t interested in buying/selling anyway

I’m still confused with what the peg actually is!

Luna’s Stabilization Role

Luna also serves as the most immediate defense against Terra price fluctuations. The system uses Luna to stabilize the price of Terra by agreeing to be the counterparty to anyone looking to swap Terra and Luna at Terra’s target exchange rate. More concretely:

When TerraSDR’s price < 1 SDR, users and arbitragers can send 1 TerraSDR to the system and receive 1 SDR’s worth of Luna. When TerraSDR’s price > 1 SDR, users and arbitragers can send 1 SDR’s worth of Luna to the system and receive 1 TerraSDR.

Flaws:

- Assumes Luna and Terra may not lose their values simultaneously

- Over-reliance on miners to stabilize/correct the system. But what if they exit? Without them, no reliable method to determine price either?

Concluding Thoughts

After reading the paper, am I more confused than I should be?

Can’t quite grasp what the system’s fundamental peg is. It feels like a mathematical balancing act between Luna, Terra, and miners to stabilize values.

And without any circuit breakers in place!

Anchor Protocol

Cyclicality in DeFi

Upswings in Ethereum’s price increase demand for leveraged long positions on Ethereum, which results in increased borrowing from stablecoin money markets. The opposite is true during Ethereum price downswings: a decrease in leveraged long demand, in combination with liquidations of Ethereum debt positions, results in less stablecoin borrowing. See the Appendix for data on this pattern collected from the past 12 months of stablecoin borrowing on Compound. The interest rate equations demonstrate the cyclicality in utilization ration directly translates to cyclicality in borrower and depositor rates. We believe that cyclicality of interest rates on DeFi protocols is a key barrier to broad adoption.

This is interesting, but how about focusing yield farming on TradFi channels, to build trust and adoption for crypto (especially stablecoins), with a strong emphasis on price stabilization?

There seems to be a heavy focus on the utilization ratio (akin to TradFi bank reserve ratios). Feels risky - it might require constant artificial APY boosts.

Anchor Rate Stability

In the absence of a printing press, Anchor uses block rewards across blockchains to derive DeFi’s benchmark rate. With Anchor, the return that depositors can expect is a function of borrowers’ on-chain income. The Anchor money market is a unique enabler of “yield transfer” from borrower to depositor by accepting bAssets on collateral. The resulting diversified yield, the Anchor Rate, reflects the market’s preferred sources of yield on the blockchain. For this reason the Anchor Rate has the potential to be more stable than any individual yield, or any fixed collection of yields.

Anchor says “market preferred yields” but isn’t this just bull market interest rate arbitrage? borrow from anchor → buy crypto → stake for rewards → profit. If cryptos crashed, people would sell and deposit stablecoins in anchor for superior APY?

Concluding Thoughts

Lesson I’m learning: Cryptos need to closely monitor yield farming activities involving their tokens. The APYs offered directly influence demand, which in turn affects the price of the crypto. Wonder how Yield Farming affects fiat pegged cryptos though 🤔

NEXT FILE

Link: /stablecoin-evaluation-framework Date: December 21st, 2024 Tags: Crypto, Payments Comments: No

Stablecoin Evaluation Framework

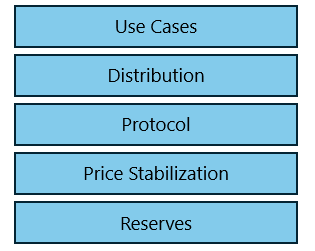

Having studied numerous stablecoins - both successful projects and notable failures - I’ve developed a broad framework to evaluate any stablecoin project. This framework examines five core components and governance.

1. Reserve Management

The foundation of any stablecoin is its reserve management system. The primary goal here is to ensure ensure liquidity and maintain user trust in the currency through effective operational practices.

Evaluation of a stablecoin’s reserves must include examining the composition of assets (whether fiat, crypto, T-bills, or other instruments) and assessing how these assets are managed to maintain liquidity. Equally important are the transparency mechanisms, (such as regular audits and third-party attestations), and the custodial structures that govern reserve access and provide bankruptcy protection.

2. Price Stability:

Price stability represents the core promise of any stablecoin. The primary objective is to maintain the target peg consistently across all market conditions.

This requires careful examination of the peg mechanism itself (whether it’s a simple 1:1 backing, an algorithmic system, or a hybrid approach) and the arbitrage mechanisms that help maintain the peg as the stablecoin is traded on exchanges. The effectiveness of these systems should be evaluated through historical performance data and stress testing.

3. Protocol

The protocol layer, through smart contracts, provides the technical foundation for all stablecoin operations. Its goal is to provide secure, efficient, and scalable infrastructure for all stablecoin functions.

Key protocol considerations include the minting and burning mechanisms, fee structures, and technical architecture. The evaluation should cover code structure, upgrade mechanisms, security measures, performance metrics, and interoperability capabilities.

4. Distribution

Distribution mechanisms determine how the stablecoin flows through the ecosystem. The goal is to ensure efficient management and monitoring of stablecoin circulation.

This includes assessing exchange coverage, geographical reach, and secondary market dynamics. A resilient distribution system should ensure preservation of the fundamentals (price stability, liquidity, etc.).

5. Use Cases

The ultimate measure of a stablecoin’s success is its utility in real-world applications. Common use cases include yield farming, portfolio diversification, payments, and cross-border transactions. The breadth and depth of use cases often indicate the stablecoin’s long-term sustainability.

Governance (Cross-cutting)

Governance frameworks underpin all aspects of stablecoin operation, from reserve management to use case development. These frameworks must clearly define:

- Decision-making authority: Whether decisions are made by the team, the community, or both

- Implementation mechanisms: How decisions are executed, whether through direct team action or programmatically through smart contracts

- Contextual variations: How governance adapts to different situations, including emergency measures and veto powers

Read: Governance Framework for DebtCoin - a stablecoin I’ve envisioned

Conclusion

This framework provides a structured approach to evaluating stablecoins. A robust project should demonstrate strength across all these areas to ensure long-term sustainability and user trust. Careful evaluation of each component helps identify potential risks and assess the overall viability of a stablecoin project.

NEXT FILE

Link: /why-stablecoins Date: December 27th, 2024 Tags: Crypto, Payments Comments: No

Why Stablecoins

As much as I enjoy exploring stablecoins, I like going back every now and then to ask myself the fundamental question: why do we even need them? While this may easily be answered by those who understand crypto, it is something I have to think about given I’m still more comfortable with the TradFi world.

Any currency needs to be judged on what it does - whether it is a unit of account, a store of value, or a medium of exchange. Memecoins offer value through humor! Bitcoin perhaps only barely ticks the store of value box, with its speculative value destined to eventually peak (either at $150K or $1M or whatever).

Well-managed stablecoins, by contrast, stand out for their lack of volatility. Their unchanging value is useful to merchants and consumers, ensuring that the worth of goods and services remains stable both before and after a transaction. They therefore excel as a medium of exchange. As a unit of account, they are unlikely to ever replace fiat. When it comes to being a store of value, I find myself conflicted.

Most stablecoins are pegged to fiat currencies, primarily the US dollar, which means their value is “tether”ed to a centralized system. If fiat itself is subject to inflation, does a stablecoin truly solve the problem of preserving value? In one sense, yes - it addresses issues like USD access and transactional efficiency, which makes it useful in regions with volatile local currencies or for cross-border payments.

But in another sense, it seems redundant. Central Bank Digital Currencies (CBDCs) aim to solve many of these same problems, arguably with more societal trust and institutional backing. Do stablecoins then, at least those that are fiat-backed, offer anything that CBDCs cannot? I’m not entirely convinced.

The perfect stablecoin would ideally be decentralized, non-volatile, and highly liquid. It would resist inflation and free people from wealth erosion caused by those controlling the money printers. This is especially crucial today, as stagnant median real household incomes may leave future generations poorer than current ones.

The perfect stablecoin would remove governments from direct monetary control, leaving them to facilitate production without the inherent conflict of doing both.

In this vein, I tried conceiving the perfect stablecoin and came up with DebtCoin - a stablecoin tied to national debt. I thought it would be relatively inflation-resistant, given how inflation and national debt can be inversely correlated. Managing liquidity and reserve growth was tricky though. Still, it was a fun thought experiment.

For now, I think stablecoins are doing what they can: they’re helping crypto take its first major strides toward real-world use cases, beyond just speculation or an instrument for the “revenge of the nerds”! They can also be a step toward breaking the monopoly of existing payment systems. Some competition and diversity in payments would be great to see.

But that isn’t the ultimate goal…— NEXT FILE — Link: /thoughts-on-stable Date: December 11th, 2024 Tags: Crypto, Payments Comments: No

Quick Notes on Stable Finance

I just explored StableFinance.io, a crypto wallet that enables users to yield farm by directly connecting with Aave.

Some initial thoughts (I’ll keep building on this):

- Lower Entry Barriers to Yield Farming: Stable allows users to connect their bank accounts, making it resemble a traditional finance (TradFi) interest-yielding app, except with potentially much higher returns.

- Simplicity: Integrated with Apple’s Face ID, simplifies self-custody for users.

- Dependence on Aave: What happens if Aave faces issues similar to Anchor?

- Differentiation: Why would users choose Stable over connecting to Aave with their original wallets? What makes it stand out?

Some ideas:

- Expand beyond Aave and USDC.

- The concept of a neobank-like wallet dedicated to stablecoins is exciting, given the growing interest in this space. How about adding features like portfolio collateral tracking? Stablecoins have different asset compositions but they are pegged to similar assets, limiting their utility as a hedge against fiat. Over time, offering users greater control to swap stablecoins may add value?

- This app seems particularly suited for TradFi users. Targeting them with educational content on stablecoins and DeFi could help bridge the gap for newcomers. Stablecoins are after all an ideal entry point for exploring DeFi. Institutional users could be another target user group

Overall, Stable seems like a promising tool for simplifying access to DeFi and making yield farming more approachable, especially for users transitioning from traditional finance.

Next, I’ll deposit some funds on Stable to see how yield farming through Aave works in practice. I’m assuming USD from bank accounts will first need to be converted into USDC within the Stable app.— NEXT FILE — Link: /quick-thoughts-on-bvnk-embedded-stablecoin-payouts Date: Febuary 11th, 2025 Tags: Crypto, Payments Comments: No

Quick Notes on BVNK Embedded Stablecoin Payouts

Fiddled around with BVNK’s developer sandbox today and went through their developer documentation. They seem to have released an embedded stablecoin payouts feature, which caught my interest given my focus on payments and stablecoins.

Jotting down quick points I’d like to clarify.

Adoption and Ecosystem Growth

- Stablecoin Adoption and Yield Farming: If stablecoin adoption grows, could this feature support more efficient account management via low-risk yield farming operators? That could boost adoption.

- New Customer Acquisition: Is this feature built to retain BVNK’s existing customers (if so, are they increasing platform fees or relying on greater fees through increased transaction volumes)? Or are they actively targeting new customer segments? — I imagine businesses in currency-volatile countries would be key targets?

- Multi-Stablecoin Support: Will BVNK eventually allow support for multiple stablecoins? That seems like a logical next step, if their customers want it.

Regulation/Resilience

- Regulatory Shifts: Stablecoin regulations seem to be evolving. What happens to this feature when shifts occur? Has this been built keeping changes in mind?

- Resilience: During events like the SVB collapse when USDC depegged, how would this system handle payouts? Could stablecoin payments continue, or would it disrupt the flow entirely?

Feature-Specific Questions

- Settlement Speeds: Curious about how fast these transactions settle. Faster than fiat? If so, I’d like to know what the tipping point for transaction times is for businesses to switch from fiat to stablecoin payments.

- Stablecoin Purchases: How are stablecoins being purchased? Are they working directly with Circle Mint or through third parties?

- Tax and Reporting: I didn’t see any tax/reporting/analytics tool integrations on the developer sandbox. Are these supported? Most businesses I’ve worked with would want these features for compliance and financial tracking.

- Compliance: BVNK’s recent features seem heavily focused on EU compliance? Wondering how much of their time and resources are going into this compared to other priorities.

- KYC/KYB Pain Points: KYC/KYB can be a real headache. How does BVNK streamline this for their EPs and EPCs? Are the flows any different for stablecoins?

Role Distinctions

I’m a bit confused about the distinctions between Embedded Partner (EP), Embedded Partner Customer (EPC), and End User. Here’s how I currently understand it:

- EP: I think of this as DoorDash, integrating BVNK’s payments into their platform.

- EPC: A restaurant listed on DoorDash (would this also be listed in the Merchants section of the platform?).

- End User: A customer ordering food through DoorDash.

This framework started making sense when I saw that payout requests come through the EP, and the EPC only gets their share after BVNK performs the USD-to-USDC exchange. Still not entirely sure, though.

Metrics!

Standard PM stuff:

- New EPCs/EPs onboarded

- Total transaction volumes

- Average transaction times

- Drop-off and failed payment rates

NEXT FILE

Link: /the-debtcoin-token Date: January 21st, 2025 Tags: Crypto, Payments Comments: Yes

The DebtCoin Memecoin

This page serves as a resource for those discovering the DebtCoin memecoin.

Note: As of February 5th, 2025, The liquidity pool for DebtCoin is now LIVE! Spend a few dollars and show your support!

Purpose of DebtCoin Memecoin

DebtCoin is a memecoin designed to fund an inflation-resistant stablecoin pegged to the U.S. national debt, serving as a critique of the United States’ profligate fiscal policy.

I created the DebtCoin memecoin to:

Gauge interest in the idea and assess whether the DebtCoin stablecoin is worth investing in.

Generate initial funds through DebtCoin memecoin fees for potential DebtCoin stablecoin development.

If the memecoin isn’t a total failure (which I expect, but hey, crazier things have happened in crypto!), I’ll commit more resources to developing the actual stablecoin, refining its mechanics, governance, and reserve management.

In short, the DebtCoin memecoin will determine whether the DebtCoin stablecoin progresses.

More about me on the homepage of this blog.

Social Channels

Expect updates to begin on Twitter and Telegram.

I use the rest of this post to summarize the concept behind the DebtCoin stablecoin I hope to build. This is essentially a consolidation of three DebtCoin posts I wrote late last year, making it easier for you to grasp the concept in one place.

Like what Seymour Durst did with the original Debt Clock in New York City in 1989, the DebtCoin stablecoin is an attempt to use crypto to highlight the growing national debt and its implications.

DebtCoin: A Stablecoin Pegged to the U.S. National Debt

Abstract

DebtCoin is a proposed stablecoin pegged to the U.S. national debt, combining stable pricing with a critique of US fiscal policy. It merges transparency with crypto’s decentralized ethos.

1. Introduction

Traditional stablecoins peg to fiat or crypto. Algorithmic stablecoins often collapse under market stress, and fiat-backed stablecoins depend on centralized entities.

DebtCoin takes a different approach. By pegging its price to U.S. national debt, it ensures relative stability, aligns with transparency principles, and highlights growing government debt.

DebtCoin offers:

Predictable pricing

Collateralized reserves

Transparent fiscal tracking

Usability for daily transactions

2. Implementation

2.1 Price Mechanism

DebtCoin’s price formula:

DebtCoin Price (USD) = U.S. National Debt / 10,000,000,000,000

For example, if the national debt is $35.92 trillion, each token is worth $3.59.

2.2 Oracle Infrastructure

A multi-oracle system fetches reliable price data from sources like U.S. Treasury Direct and the Federal Reserve, using median-based calculations to filter anomalies.

2.3 Reserve System

DebtCoin ensures security and transparency through:

100%+ collateral in USD

Real-time proof of reserves

Regular third-party audits

2.4 Minting Mechanism

Tokens are minted upon deposit and burned upon withdrawal, ensuring controlled supply.

3. Reserve Management

3.1 Rollout

DebtCoin will launch with an ICO, offering tokens at a discount (e.g., 90% of debt value). Initial proceeds will fund operations and currency development. Restrictions like throttled selling will prevent rapid profit-taking.

At launch, reserves won’t be 1:1. The short-term goal is parity; the mid-term goal is exceeding it. Funds will be allocated to low-risk assets like Treasury bills and TIPS, ensuring liquidity and stability. Transparency via real-time tracking and audits will build trust.

3.2 Scenario Handling

Here’s how DebtCoin could handle potential scenarios.

Scenario 1: Rapid Debt Increase

High Liquidations: Holders may sell to secure profits. A phased liquidation approach (e.g., partial payments over two weeks) and dynamic transaction fees can mitigate risk.

High Purchases: New buyers may rush in. The system must handle rapid minting and potential future sell-offs.

Scenario 2: Rapid Debt Decrease

High Liquidations: Easier to manage with strong reserves.

High Purchases: If reserves deplete and debt rises again, liquidity challenges may emerge.

Stress tests will simulate extreme events (e.g., wars, inflation) to ensure resilience.

3.3 Long-Term Goals

DebtCoin aims to diversify reserves into:

Commodities: Gold and metals for inflation hedging

Global Currencies: Reducing USD dependency with Euro, Yen, etc.

Crypto Assets: Low-volatility digital assets

Treasury Inflation-Protected Securities (TIPS)

Expanding reserves could enable advanced features like yield farming and payment systems.

4. Governance Framework

4.1 Immutable Components

Core features locked into the protocol:

Price formula (Debt/10T)

Minting/burning mechanics

Security framework

Oracle integration

4.2 Upgradeable Protocol Parameters

Adjustable settings via on-chain voting:

Reserve Ratios: Initially 100% USD-backed, adjustable over time

Transaction Limits: Caps on minting and burning

Fees: Dynamic (e.g., 1%) to support operations

Oracle Settings: Data weighting and validation

Emergency Protocols: Circuit breakers (e.g., 24-hour minting pause)

4.3 Hybrid Governance

A mix of off-chain discussions and on-chain execution:

Reserve Composition: Community proposals for new assets (gold, crypto)

Liquidation Procedures: Debated off-chain, implemented on-chain

4.4 Emergency Powers

For critical situations:

Emergency Pause: Suspend operations in crises

Multisig Control: Consensus-driven decision-making

Strategic Oversight: Ensuring long-term alignment

5. Conclusion

DebtCoin integrates security, transparency, and usability while critiquing fiscal policy. Features like yield farming, lending, and liquidity solutions position it as a next-generation stablecoin.

By merging transparency with practical applications, DebtCoin aims to redefine stablecoin utility and governance.

NEXT FILE

Link: /best-use-case-cross-border-stablecoin-payments Date: March 21st, 2025 Tags: Crypto, Payments Comments: Yes

Best Use Case for Cross-Border Stablecoin Payments

Cross-border payments encompass four primary use cases: B2B, C2B, B2C, and C2C. Each implements different operational models, such as traditional banks using SWIFT and currency swaps or remittance providers like Wise using optimized local settlement models.

Stablecoins present an opportunity for disruption, but their utility differs by scenario. Here’s an analysis of existing TradFi cross-border solutions based on cost, time, ease of use, CLV/CAC* and transaction volumes (based on my personal understanding, not backed by data).

| Parameter | B2B (Payments) | C2B (Collections) | B2C (Payouts) | C2C (Remittances) |

|---|---|---|---|---|

| Cost | Low | Moderate | Moderate | High |

| Time | Slow | Moderate | Moderate | Fast |

| Ease of Use | Complex | Moderate | Moderate | Simple |

| CLV/CAC | High | Moderate | Moderate | Low |

| Volume | High | Moderate | Low | Low |

Why B2B is the Best Fit for Stablecoin Payments

1. Payment Orchestration

In B2B payments, orchestrating cross-border transactions is inherently complex, as companies must navigate multiple currencies, regulatory frameworks, and financial institutions. Stablecoins address this by streamlining the process through partnerships with specific liquidity providers in regions where fiat-stablecoin swaps are common.

These tie-ups handle the on-ramp and off-ramp requirements seamlessly, reducing the need for multiple intermediaries and enabling businesses to bypass traditional banking rails. For example, in corridors like USD-CAD or EUR-GBP, with high stablecoin liquidity potential and low currency volatility, these solutions can offer reliable and efficient transaction pathways.

2. Financial Efficiency

Stablecoins reduce costs and delays by bypassing intermediaries like SWIFT and correspondent banks. Integrating yield farming solutions with crypto wallets could allow businesses to optimize idle funds, enabling more efficient money management. These wallets can also facilitate access to on-chain lending, providing businesses with quick, low-cost financing options, further enhancing the appeal of stablecoins.

3. Industry Niches and Referral Potential

A focused entry into tech-savvy industries like ecommerce or SaaS allows stablecoin providers to grow via referral networks. Once one company adopts the model, their domestic suppliers and clients are incentivized to join, further scaling adoption. Over time, business tools such as tax management and invoicing can be integrated.

4. Trust and Security Measures

While trust in stablecoins remains a concern, this can be mitigated through audits, insurance guarantees, and partnerships with entities ensuring zero-liability solutions. Such measures mirror the protections already familiar to consumers via payment networks like Visa and Amex.

Why C2C (Remittances) Faces Challenges

Remittances dominate forex narratives but have small volumes and face stiff competition. Companies like Wise have fine-tuned batching models and streamlined local currency settlements to minimize costs and time, making it difficult for stablecoins to offer a compelling advantage. Even with trust and efficient infrastructure, breaking into this space poses significant hurdles for stablecoin solutions.

Conclusion

Stablecoin payments hold the most promise in the B2B sector, where the gap between TradFi and DeFi is largest. By targeting specific geographies, focusing on payment orchestration and leveraging existing industry trust mechanisms, stablecoins can become a game-changer for global business transactions.

CLV/CAC: Customer Lifetime Value / Customer Acquisition Cost

I wrote this post expanding on Matt Brown’s Cross-border Payments in ~1,000 Words — NEXT FILE — Link: /should-card-rewards-banned Date: February 21st, 2024 Tags: Payments Comments: No

Should card rewards be banned?

Imagine you don’t own a credit card and shop for $100 of groceries using a debit card. The supermarket pays a $1 interchange fee to payment networks like Visa or Amex, reducing its revenue to $99. This fee is split between the network and banks to cover processing costs.

Now consider a premium rewards cardholder making the same $100 purchase. The payment network provides $2 in rewards points, so it charges the supermarket $3 in interchange fees, leaving them with $97. To offset this loss, the supermarket raises prices, making the $100 purchase cost $102. The debit card user pays the full $102, while the rewards cardholder effectively pays $100 after receiving points.

Scale this, consider the 2X, 3X, 5X rewards on plush services like airlines, gas and streaming services and you see how reward points are made possible through higher interchange fees, leading to price increases paid for by lower-income consumers.

Should card rewards therefore be banned?

I’m skeptical of regulation. Even well-meaning regulations often have unintended consequences. Markets tend to self-correct. For example, interchange regulations in the EU, Australia, and Canada haven’t significantly reduced prices. Instead, banks offset losses by raising other fees, like annual or foreign transaction fees.

A better approach may lie in pricing transparency. Card companies could provide detailed billing statements showing fee breakdowns. Consumers would learn how much of their spending reaches merchants versus intermediaries.

Over time, this awareness could encourage merchants to disclose interchange fees separately, rather than embedding them in prices. Uniform card holds exceeding the sale price could offer a temporary solution until fees are calculated and shared with consumers.

Premium cardholders would see how much their rewards cost compared to other payment methods. Informed, they could weigh rewards against extra costs.

The result would maintain current pricing mechanisms while eliminating the regressive redistribution of costs. Rewards points would become more market-optimal, fair, and ethical.— NEXT FILE — Link: /mountain-protocol-usdm-questions-ideas Date: February 21st, 2025 Tags: Crypto, Payments Comments: Yes

Mountain Protocol - USDM Questions and Ideas

This post presents questions and thoughts I have after reviewing the Mountain Protocol Documentation. Additionally, I explore potential structural changes to USDM, big-picture implications of stablecoins, and future directions for Mountain Protocol.

30-Second TL;DR

- Should USDM’s peg fluctuate based on yield rewards instead of staying at 1:1? Could this simplify rebasing, change how users time their investments, and improve the coin’s utility?

- Are stablecoins really decentralized, or is everything still built on Traditional Finance? Even algorithmic stablecoins rely on fiat-based stablecoins - so where does DeFi really begin?

- What happens if the S&P 500 launches a stablecoin? Wouldn’t it be classified as a security? Aren’t all yield-bearing stablecoins securities? Did Gary Gensler have a point?

- Is Circle’s USDC model extractive? While inflation hurts holders, it benefits Circle’s owners through superior yield - does USDM present a fairer alternative?

- What’s next for USDM? Can it expand through PSMs, LPs, and fiat on/off ramps to become a superior base stablecoin?

- How should USDM reserves be stress-tested? Could a risk-hedging agent profit when stablecoins face crises like USDC’s SVB depeg?

Table of Contents

- Yield & Market Dynamics

- Stablecoin Classifications & Systemic Risk

- USDM’s Future & Competitive Positioning

- Reserve Management & Stability

Yield & Market Dynamics

Should USDM’s peg fluctuate with yield rewards? Would this affect user behavior, simplify rebasing, and improve integrations in LPs & PSMs?

Should the Peg Fluctuate Instead of Minting New Tokens?

This means:balanceOf(account)USD = balanceOf(account)USDM * (USD/USDM peg), where USD/USDM peg is always 1:1 on Mountain’s platform and held through arbitrage on secondary markets.

But what if the peg fluctuates based on the rewardMultiplier?

If we redefine the equation as USD/USDM peg = rewardMultiplier,

Then, balanceOf(account)USD = balanceOf(account)USDM_Proposed * (USD/USDM peg).

Ensuring balanceOf(account)USDM_Proposed = shares[account].

- Right now, USDM uses a 1:1 peg, with rewards distributed separately.

- Could rewards be baked into the peg itself, eliminating the need to mint new tokens?

- Would this change how users time their purchases—like wanting to buy into the S&P 500 earlier rather than later?

- Would it make rebasing less technically complex, especially for wUSDM?

Liquidity & Arbitrage Considerations

- Would a fluctuating peg make USDM easier to integrate into liquidity pools (LPs) and peg stability mechanisms (PSMs)?

- If this system is too complex, could another linked token be created where the price fluctuates instead of USDM?

Low-Yield Environments

- If Treasury yields decline, how does USDM remain attractive?

- Does Mountain expect circulation to fluctuate with yield levels, or are alternative strategies in place?

When is “Day 0” for USDM?

- When exactly does USDM’s lifecycle begin—is it the day it’s minted, transferred, or reset with each transaction?

Stablecoin Classifications & Systemic Risk

Are stablecoins actually decentralized, or is everything still dependent on TradFi? If major financial indices launched a stablecoin, would it be classified as a security?

What if the S&P 500 Launched a Stablecoin?

- Would it be classified as a security?

- How does this compare to USDM’s classification?

Is DeFi Just Traditional Finance in Disguise?

- Even algorithmic stablecoins ultimately rely on collateralized stablecoins.

- Are all stablecoins just TradFi wrapped in a DeFi interface?

- If governments still back everything, but markets make the decisions, is this the real definition of DeFi?

- Could current stablecoins unlock efficiency gains?

USDM’s Future & Competitive Positioning

Can USDM replace USDC as a fairer stablecoin? What integrations (PSMs, LPs, fiat rails) will drive its long-term adoption?

The Non-Extractive Model — A Better USDC?

- USDM is not extractive, unlike USDC, where Circle’s owners pocket all the yield.

- Circle profits from inflation—as interest rates rise, its yield grows, while USDC holders lose purchasing power.

- Wouldn’t it be better if USDM replaced USDC as the default stablecoin?

What’s Next for USDM?

- Mountain seems focused on:

- Swap pools

- Lending market integrations

- PSMs for stablecoin swaps

- LP adoption for yield farming

- Swap pools

- PSMs and LPs are likely the core use cases, while swaps & lending require higher volumes than USDM currently has.

- Expanding native USDM on multiple blockchains could accelerate adoption.

Fiat Rails & Diversification Beyond USDC

- Can USDM add fiat on/off ramps to convert fiat directly into USDM? It might serve as a good use case for cross-border-payments

- Should USDM diversify beyond USDC, given its single point of failure risk?

- Would this make USDM a more sustainable base stablecoin?

Reserve Management & Stability

How does Mountain Protocol manage liquidity and risk? Can stress-testing stablecoins unlock new profit opportunities?

Liquidity & Maturity Management

- What processes and automations does Mountain Protocol use to manage the weighted average maturity (WAM) and weighted average life (WAL) of USDM reserves?

- What does the USDM minting-to-reserves workflow look like?

Reserves Attestation & Stress-Testing Risks

- Could a new risk-hedging agent profit by arbitraging stablecoin depegs?

- For example, if USDC loses its peg due to a banking crisis, could this agent trade around such events?

- Can this agent detect interlinked risks, like USDM holding USDC, which in turn may rely on the same banks as USDM’s reserves?

- Could DebtCoin hedge against U.S. debt servicing risks in the unlikely case of government defaults?

Final Thoughts

Stablecoins are evolving, and USDM is proof that there’s plenty of room for innovation beyond USDC and USDT!

—

NEXT FILE

Link: /stablecoin-payments-aggregation-dynamic-auctions-zero-liability Date: April 11th, 2025 Tags: Crypto, Payments Comments: Yes

Stablecoin Payments Aggregation Through Dynamic Micro Auctions and Zero Liability Protection

I’ve been thinking about persistent pain points in stablecoin payment orchestration, particularly in non-US corridors where onramp/offramp complexities arise due to immature crypto-fiat liquidity. Stablecoin payments, after all, seem like the perfect catalyst for driving institutional crypto adoption.

My idea? Inject market dynamics by holding mini auctions at every critical node of a transaction. The mechanism is simple: let liquidity providers bid in real time - addressing cost, speed, and trust issues - while a robust zero liability framework ensures that any fraud or failure is covered by the payments aggregator, not the user or liquidity provider.

The Dynamic Micro Auction Approach

Stablecoin payments can be executed through eight potential transaction pathways consisting of four key nodes:

- The buyer’s fiat bank account

- The buyer’s crypto wallet

- The seller’s crypto wallet

- The seller’s fiat account

For each node, the aggregator maintains a corresponding account. For example, in a USD/EUR corridor, the aggregator would operate:

- a USD fiat bank account

- a USDC crypto account

- a EURC crypto account

- a EUR fiat account

For optimal experience, KYC and verification are handled by the aggregator.

Overall Flow:

Request for Bids:

Suppose a user wishes to transfer funds from their USD account to a seller’s EUR account. The user specifies the amount to be transferred, and the aggregator issues a Request for Bids.Bidding:

Liquidity providers submit bids with their best price and time commitments. The aggregator ranks these bids and presents the top options (e.g., 1.5% immediate, 0.8% in 24 hours) to the user - without revealing the providers’ names. The user then selects the option that best meets their needs.Settlement:

Funds are transferred from the buyer’s USD account to the aggregator’s USD account. Next, the funds are converted to the aggregator’s USDC wallet (which can be done in batches for efficiency). The funds are then swapped with the liquidity provider, who sends them to the aggregator EURC wallet. Finally, the funds are transferred either to the seller’s EUR fiat account or remain in the EURC wallet, based on the buyer’s request.

Buyers will quickly realize that fiat-to-fiat transfers incur higher fees than crypto-to-crypto transactions, encouraging them to hold more funds in stablecoins. This shift can spark a virtuous cycle of improved rates, enhanced liquidity management, and the proliferation of additional crypto services. A shift from USDC to inflation-resistant stables such as the now-acquired USDM may also be a good thing.

Risk Scoring

Over time, as bids are processed and success rates recorded, providers can be scored and dynamic pricing implemented, thus incentivizing strong performance. Since the overall liability for delivering payment to the supplier’s wallet rests with the aggregator, aligning risk with liquidity providers’ incentives is crucial. The aggregator’s primary responsibility will be acquiring buyers and sellers and ensuring a seamless user experience while allowing providers to compete on the backend. Risk is continuously monitored using a variety of metrics.

After each transaction, performance data is fed back into the system to refine risk scores and future auction parameters. This constant feedback loop enables the network to learn and adapt, ensuring continuous improvement.

Final Thoughts

This approach harnesses real-time market dynamics to make stablecoin payments more efficient and resilient. By combining dynamic micro auctions with zero liability protection, we can optimize for cost, speed, and trust while ensuring that any failures are absorbed by the aggregator - not the end user. Inspired by models in insurance, supply chain routing, payment card liability protections, and travel aggregators (and a dynamic interchange pricing patent I co-invented), this is a shift from traditional models and could be a step toward a more robust global payments network.

NEXT FILE

Link: /fiatized-stablecoins Date: March 11th, 2025 Tags: Crypto, Payments Comments: Yes

Fiatized Stablecoins

There’s been a transition in the crypto space from decentralized currencies like Bitcoin to fiat-pegged stablecoins. We’re now witnessing the next transition - what I call the shift from “extractive” stablecoins (where a rise in inflation raises the yield on these coins, enriching the issuers while making holders poorer) to yield-bearing stablecoins. I believe we’re only at the beginning of this shift and that this might just be the major crypto breakthrough that brings it into mainstream banking.

Stablecoins function similarly to ETFs in that they have separate layers for reserves and crypto protocols. The reserves are typically managed and invested in cash and treasuries, while smart contracts facilitate the minting and burning of tokens. These two layers are connected through careful liquidation processes and mechanisms.

The problem with stablecoins though is that they remain too technical for the average user.

I’ve been thinking of something I call “fiatized stablecoins” (as opposed to tokenized assets or deposits) to further bring the advantages of crypto into the mainstream. I don’t particularly care about most developments in the crypto space - they’re fun to analyze, but beyond that, what I’m personally driven by is crypto’s potential to prevent median wealth erosion due to inflation, a challenge that societies, both rich and developing, constantly face.

To illustrate fiatized stablecoins, let’s consider a mobile app called “Simple”.

Consider this user flow:

User Interacts with App

- The user initiates an action (e.g., deposit, withdrawal, transaction).

App Interacts with Simple’s Fiat Bank Account

- The app executes the user’s actions and connects to a fiat bank account owned by Simple.

- This can involve ACH, wire transfers, or card payments.

Simple Interacts with Stablecoin Protocol

- Simple owns a crypto wallet (or a set of crypto wallets, whichever is more secure from an operational standpoint) that has access to a yield-bearing stablecoin’s protocol layer — let’s use Mountain’s USDM as an example, a crypto I’m personally a fan of.

- Simple can interact directly with the stablecoin issuer to mint or burn stablecoins as needed.

Stablecoin Issuer Manages Reserves

- The stablecoin issuer (e.g., Mountain) independently manages underlying fiat reserves, compliance and redemption processes, ensuring that all circulating stablecoins (and therefore, all Simple’s fiat deposits) are properly backed.

Essentially, just as stablecoin issuers centrally operate reserves that are invested in treasuries, Simple will centrally operate the wallet that interacts with the stablecoin protocol. Simple’s fiat money management can be optimized through streamlined batching and settlements. If Simple ensures that it always has more stablecoins in its crypto wallet than circulating fiat, it should have room to slow down settlements in favor of quicker user deposits/withdrawals.

The idea is to therefore have a fiat layer on top of the stablecoin layer, which itself sits on top of another fiat layer—bringing it as close to the regular end-user as possible. Picture an app that allows users to buy stablecoins with their cards and bank accounts. I’ve shared a few basic prototype screenshots so I could visualize this concept.

Why does this matter?

Whatever crypto’s promise has been, it hasn’t succeeded in widespread adoption simply because it is too complex (note: institutional adoption isn’t the same as widespread adoption). The biggest crypto successes haven’t necessarily been decentralized. In fact, 80% of all crypto transactions happen with stablecoins, suggesting that crypto is perhaps more linked to government actions than ever before. It’s also telling that the most successful companies in the space haven’t been decentralized entities but centralized firms that offer a certain level of trust-Coinbase, Circle, etc.

I argue that the key differentiator in the crypto space, just like in the rest of the world, comes down to trust and simple design. Which is why I believe an app that keeps all the complexities of crypto under the hood - with no mention of wallets or chains - could be a breakthrough. The goal is to target regular banking users who simply want low-risk, better yields on their daily expenses and who might be more likely to replace their checking and savings accounts with Simple.

While the rebasing mechanism would ensure that the value of their money increases, if Simple’s wallet can engage a tiny portion of its tokens in DeFi staking, the money earned could potentially exceed the actual rebasing yield of the stablecoin.

Regulatory Concerns

The challenge with this approach is that it blurs the lines between HYSA neobanks and stablecoins. A service like Simple is almost indistinguishable from a high-yield savings account. The differentiation will ultimately come down to policy. Governments have yet to classify yield-bearing stablecoins as securities. It therefore is difficult to categorize an app like Simple as a security since it only interacts with stablecoins. However, it also doesn’t fully escape the Howey Test, as there is a clear expectation of profit.

Moreover, for a fiatized stablecoin like Simple,

- Are we a fintech company like Chime?

- Are we a Money Services Business (MSB) like Circle?

- What registrations would we need - FinCEN, SEC, FINRA, FDIC?

I believe there is something here and I want to explore it further. If you have thoughts or more information, let me know.

NEXT FILE

Link: /weighing-in-stablecoin-debate Date: June 11th, 2025 Tags: Crypto, Payments Comments: Yes

Weighing in on the Stablecoin Debate

In the last few weeks, there’s been a lot of chatter about whether stablecoins offer anything beyond regulatory arbitrage. Critics argue they’re just slick wrappers around fiat, used to dodge capital controls or skirt around legacy infrastructure. And beyond use cases in high-inflation or emerging economies, they don’t offer much. But I think the real potential of stablecoins lies in eliminating that divide between banking and finance.

Say you send me $50 after dinner, that money just sits there. Why shouldn’t it be auto-invested into a low-risk, on-chain ETF the second it hits my wallet? Why shouldn’t I be able to redeem or spend it instantly too?

Yield-bearing stablecoins felt like a first step in that direction. But after conversations with yield-bearing stablecoin issuers (like the now-acquired USDM team) and some deeper research into smart contract design, I quickly realized how operationally complex this was. The mechanics of distributing yield across tokens that are constantly moving between wallets is messy. And that’s before you even get to the legal questions - are they securities or not?

Maybe the path toward merging banking and finance doesn’t begin with merging payments and finance? Maybe we need some clear lines, like a stablecoin that’s purpose-built for payments and another for investing. Through conversations I’ve had with teams at Circle, I learnt about something along those lines: users accept USDC payments, have their tokens auto-converted on Coinbase into yield-bearing assets like USDY. That kind of flow moves us in the right direction.

But it still isn’t the whole picture! The real unlock would be a system that blends the ease of Venmo with the investment rails of Robinhood, where money both moves and grows without friction and liquidity management is managed efficiently in the background and users barely notice.

There’s been real progress in the last few months. Wallets are getting more user-friendly: better abstraction, better UX. Payments teams are already building on this. So are stablecoin-native retail trading apps. When all these pieces click together, we might actually get to that integrated Robinhood-Venmo world. And bringing those stablecoin use cases into the real world is what we’re building toward at Miruvor.

NEXT FILE

Link: /mondeum-cross-border-stablecoin-exchange Date: June 21st, 2025 Tags: Crypto, Payments Comments: Yes

Mondeum: A Model for a Cross-Border Multi-Fiat Stablecoin Exchange

This concept note outlines a new model for a cross-border stablecoin exchange where all trades are routed through Mondeum, a global basket token backed by fiat currency stablecoins from around the world. It introduces a three-layered system to separate token risk and treasury risk and manage pricing and liquidity. The goal is to enhance swaps between stablecoins backed by different fiat currencies and lay the foundation for the next phase of stablecoin adoption. We walk through the rationale, architecture and rollout roadmap.

Read the Concept Note →

NEXT FILE

Link: /can-card-rewards-more-contextual Date: March 21st, 2024 Tags: Payments Comments: No

Can card rewards be made more contextual?

Have you ever felt that the reward points offered by your card issuer don’t reflect your consumption habits? Could there be a way to make these rewards more ‘contextual’ and encourage you to shop at local businesses?

Say a card issuer triangulates where you live based on your payment history. It wouldn’t need your mobile GPS data but could analyze ‘physical’ transactions you typically make near your home. By examining purchases like groceries, gas, or medicine, the issuer can leverage merchant zip codes to estimate your living area.

Next, the issuer analyzes your transaction history, predicting the Merchant Category Codes (MCCs) you favor for frequent or high-value purchases.

For each identified zip code, the issuer compiles a list of top merchants by MCCs, chosen based on criteria like transaction volume or low chargeback risk.

Using data about your preferred MCCs and top MCCs in the area, the issuer estimates which merchants you might transact with given an increase in rewards points. The issuer introduces a rewards offer, notifies you through your preferred channel, and specifies a duration for the offer, encouraging transactions with local merchants.

From a cardholder’s perspective, this system offers several benefits. Rather than generic rewards, users receive personalized offers based on their shopping habits and location, potentially boosting satisfaction.

Merchants, especially local businesses, can increase traffic and sales by joining such a contextual rewards program. Personalized incentives help attract and retain customers.

Issuers can use this solution to improve user loyalty and drive transactions toward preferred merchants. This also allows merchants to advertise themselves. Data insights help refine rewards strategies, differentiate programs, and boost interchange revenue.

In conclusion, this solution proposes making reward programs more contextual and personal. It benefits cardholders, merchants, and issuers by enhancing rewards programs and aligning incentives with individual shopping behaviors.

NEXT FILE

Link: /are-digital-payments-wiping-out-economy Date: April 21st, 2024 Tags: Payments Comments: No

Are digital payments wiping out the economy?

In today’s digital age, money flows frictionlessly from one digital transaction to another. Invisible to consumers though, is a contentious commission called the “interchange fee” that banks and payment networks levy for each transaction processed.

Imagine making a $50 purchase using your credit card. The merchant pockets $49, after losing about 2% in interchange fees. When the merchant spends that $49 with another seller, another 2% is lost. Extrapolate this, play this out for a hundred exchanges, and your initial $50 dwindles to a mere $5. The rest is gobbled up by the banking system, resulting in 90% of the original monetary value ostensibly disappearing into financial ether.

In the face of this gradual erosion, a pertinent question arises: Are digital payments even worth it? Why shouldn’t cash still be king when digital payments clearly don’t make economic sense?

Naturally, the sequential transaction model I’ve drawn oversimplifies real-world economics. First, digital payments aren’t as uniformly costly as I’ve made them seem. Some exchanges, like card transactions over the internet, can indeed cost over 2% of a purchase. Others, like bank transfers between merchants, cost much less. This is critical considering that most subsequent transactions from the initial $50 purchase are unlikely to involve cards.

Moreover, as we progress up the payments chain towards larger entities like corporations, transactions start to aggregate. Just as a retail store procures goods in bulk from a wholesaler, corporations transact in large volumes with their suppliers. In other words, it costs much less to process a $50,000 transaction once than it does to process a thousand $50 transactions. Working out the exchange of money through a sequential transaction model therefore doesn’t make sense.

Even if such a model did hold true, consumers regain a significant chunk of the money lost to interchange through rewards points, debunking the 2% value erosion assumption.

Next, despite its drawbacks, digital payments have revolutionized transactional behavior. Would you have made that $50 purchase in the first place had it not been for the convenience of your credit card? Greater transactional frequency doesn’t just shift money, it stimulates value creation within the economy. It also helps to view interchange as a valuable service, not a mere cost. Would you rather lose hours of your time (and as a result, economic output) visiting multiple shops or pay that 2% to purchase multiple items with a few clicks on Amazon?

Lastly, does the banking system really “gobble up” money? Interchange fees charged by banks and payment networks are channeled back into the system, bolstering availability of credit, which when judiciously distributed, aids in value creation. Moreover, imagine a physical $50 bill changing hands a hundred times and consider the expenses tied to its transport, storage and security. A digital transaction of $50 doesn’t lose its value. Rather, its worth amplifies.

NEXT FILE

Link: /why-india-upi-will-fail Date: May 21st, 2024 Tags: Payments Comments: No

Why India’s UPI will fail

UPI (Unified Payments Interface) has transformed India’s economy, enabling seamless transactions across markets, offices, and homes. Indians use it for everything from paying bills to making purchases, bypassing the “cards phase” of payments by jumping directly from “cash” to “mobile.”

But is UPI truly a success? While widely adopted, its long-term sustainability is questionable.

Zero-MDR Model

UPI’s zero-MDR (Merchant Discount Rate) policy is key to its appeal. Unlike Visa or Mastercard, which charge interchange fees of over 2.5% per transaction, UPI is free for merchants. However, these fees fund operational costs, infrastructure, and fraud prevention for global payment networks. UPI’s high failure rates reflect insufficient investment, a direct result of its zero-MDR model.

Lack of Innovation Incentives

UPI is owned by NPCI, a government nonprofit. Historically, profit-driven companies have pioneered payment innovations like EMV chips and NFC payments. Can a nonprofit spearhead future advancements like biometrics or cryptocurrencies? Indian banks also lack incentives to innovate, as they earn nothing from UPI transactions.

Winners and Losers

UPI has hurt local players like Paytm, which once led India’s payments space but has lost users to UPI. Ironically, UPI’s biggest beneficiary is America’s Google, whose app gathers valuable commerce data from Indian users. So much for Atmanirbharta (self-reliance).

Missed Opportunities

Without UPI, Paytm might have leveraged India’s growing economy to expand globally, much like Visa and Mastercard. A less interventionist policy, akin to the EU’s PSD2, could have fostered competition without stifling innovation. Instead, India’s reliance on government-led solutions mirrors past missteps with state-owned airlines, banks, and telecom operators.

Conclusion

While UPI enables fast, free transactions, its zero-MDR model, lack of innovation incentives, and unintended consequences for local players raise doubts about its sustainability. For all its success, UPI risks becoming another example of myopic policy prioritizing short-term conveniences while undermining long-term progress.— NEXT FILE — Link: /can-payment-cards-answer-online-safety-conundrum Date: June 21st, 2024 Tags: Payments Comments: No

Could payment cards answer the online safety conundrum?

The quest for a safer internet, especially for children, often leads to discussions on digital age verification. Legislators worldwide are proposing measures to mandate online age verification. Simple solutions like ticking a box or parental control tools may soon be replaced by stricter systems. Will uploading a government ID become necessary for activities like buying alcohol online or watching R-rated content on Netflix?

Age verification naturally spark privacy concerns. Social media platforms are exploring AI and facial recognition algorithms to estimate age via selfies, avoiding the need for government IDs. However, storing biometric data comes with risks, including misuse and breaches.

Could payment cards offer a better balance between privacy and safety?

Imagine a scenario where payment cards could discreetly verify age without revealing personally identifiable information to online merchants. When a user enters card details online, the website contacts the card issuer to confirm if the user is above a certain age (e.g., 18). The issuer responds with a simple “yes” or “no,” without sharing the user’s exact age. This preserves privacy, ensures safety, and requires no extra effort from users.

Likewise, digital passes like Allpass offer non-payment card alternatives. Users could buy an “age pass” in retail stores, with cashiers verifying their age by checking IDs before issuing the pass. Websites would accept these untraceable passes for access.

These solutions are not foolproof. The goal here is to simply explore methods balancing privacy and safety. As the virtual and real worlds converge, and identity verification grows, refining such solutions becomes critical.— NEXT FILE — Link: /redefining-payments Date: August 21st, 2024 Tags: Crypto, Payments Comments: No

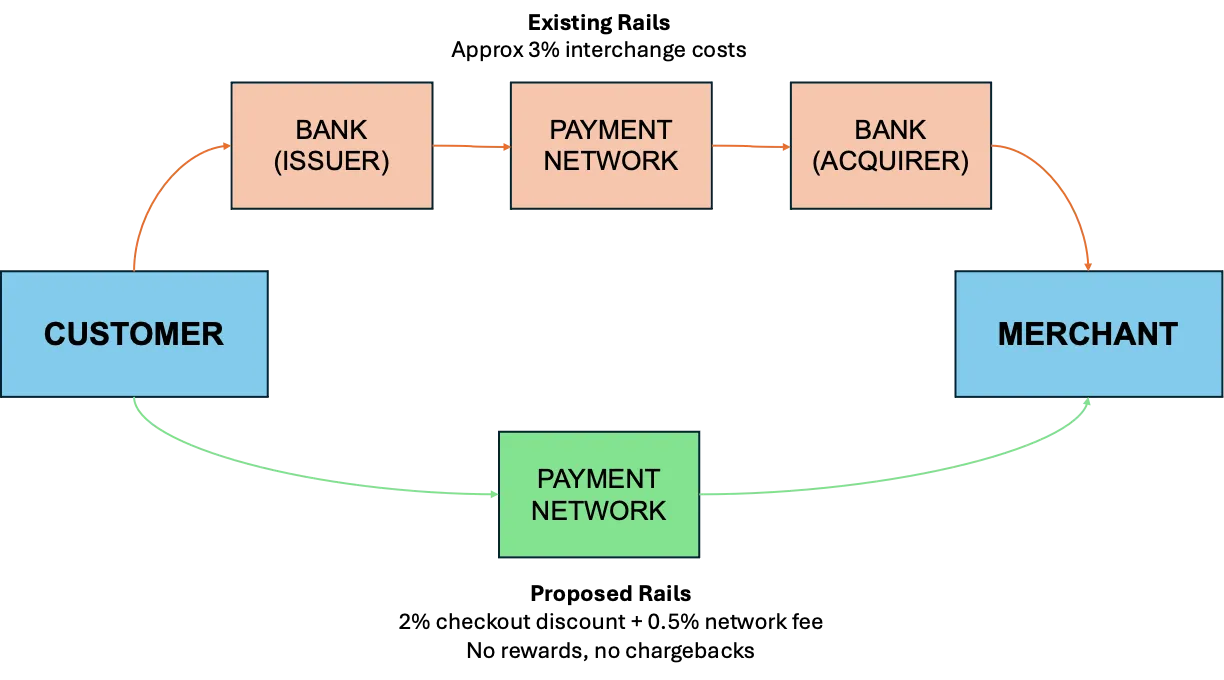

Redefining Payments: A Smarter Future for Merchants and Consumers

Today’s payment system is bloated and dominated by entrenched interests. This article proposes a crypto-based framework to eliminate banks and payment networks as intermediaries, solving issues like high interchange fees that burden merchants.

Current System Challenges

Users today obtain credit/debit cards from “issuing banks” who partner with payment networks (e.g., Visa, Amex). Merchants receive funds through “acquiring” banks. Banks and payment networks control liquidity and money flow, making the system vulnerable to censorship, inefficiency, and privacy risks.

The structure is sustained by a convoluted web of interchange fees and reward programs, which disadvantage merchants. Existing cryptocurrency systems, while effective for P2P payments, lack widespread adoption due to usability challenges.

Proposed Solution

The proposed system leverages cryptocurrency for direct payments. Users get immediate discounts at checkout for using crypto, bypassing interchange fees and card rewards. Merchants pay a 0.5% network fee, while users enjoy a flat 2% “checkout discount”.

Merchants currently pay around 3% in fees plus costs from fraud and chargebacks. The new system eliminates these inefficiencies. The proposed system will need to acquire both users and merchants, similar to Amex or Discover models.

Implementation

Authentication: The system verifies user account balances. If funds are available, the merchant is authorized to complete the sale. Chargebacks will not be supported for operational efficiency. Users will use a QR code, PIN, or phone locks for security.

Sale: The system benefits merchants with no interchange fees, no chargebacks, and reduced costs. User adoption may take time as cardholders are used to rewards programs. Efforts such as the Payment Card Interchange Fee Settlement provide a framework for advocating merchant-friendly policies.

Clearing and Settlement: Settlements will occur in daily batches. This ensures faster processing and eliminates chargeback risks.

Currency: Stablecoins can address volatility concerns. Same-day clearing and fiat conversion will incentivize merchant adoption. Delta-zero stablecoins could be explored in the long term.

Challenges

Adoption requires overcoming entrenched habits, trust issues, and evolving regulations. Fraud and lack of chargebacks may deter users. Legacy players might lower interchange fees to compete.

Future Vision

The rollout will prioritize small businesses and POS payments. An open ecosystem for merchant tools will drive innovation. P2P loans could expand the model to include credit. A fixed 2% discount will attract users, giving this system a competitive edge.

Finally, raising awareness of high-reward cards’ unfair impacts can promote a more equitable payment system.— NEXT FILE — Link: /debtcoin-stablecoin Date: November 20th, 2024 Tags: Crypto, Payments Comments: No

DebtCoin: A Stablecoin Pegged to the United States National Debt

Abstract

DebtCoin is a stablecoin I propose that is pegged to the U.S. national debt, serving as a transparent crypto token that tracks arguably the world’s most significant economic metric. It combines the stability of traditional stablecoins with a critique of U.S. fiscal policy.

Introduction

Stablecoins traditionally peg to assets like fiat currencies or cryptocurrencies. Algorithmic stablecoins often fail under market stress, while crypto-backed tokens are volatile. Fiat-backed stablecoins depend on centralized systems, contradicting crypto’s decentralized ethos.

DebtCoin provides a different approach. By linking its value to the U.S. national debt, it ensures stability, aligns with crypto’s transparency principles, and highlights the growing government debt.

DebtCoin offers:

- Predictable pricing

- Collateralized reserves

- Transparent tracking of fiscal metrics

- Usability for daily transactions

Implementation

Price Mechanism DebtCoin’s value is calculated as:

DebtCoin Price (USD) = Current U.S. National Debt / 10,000,000,000,000

So at $35.92 trillion in national debt, each token would be worth $3.59.

Oracle Infrastructure A multi-oracle system provides reliable price data, using sources like U.S. Treasury Direct and Federal Reserve Economic Data. Median-based calculations detect and exclude anomalies.

Reserve System DebtCoin ensures security and transparency with:

- 100%+ collateral in USD

- Real-time proof of reserves

- Regular third-party audits

Minting Mechanism

Tokens are minted upon deposit and burned upon withdrawal, maintaining supply control.

Conclusion

DebtCoin combines strong security, reliable price feeds, and practical use. It critiques fiscal policy while offering features for yield farming, lending, and liquidity. DebtCoin aims to redefine stablecoins, blending functionality and transparency in an innovative way.

This is the first article in a 3-part series on DebtCoin:

DebtCoin: A Stablecoin Pegged to the United States National Debt (current)

DebtCoin: Reserve Management

DebtCoin: Governance Framework -– NEXT FILE — Link: /debtcoin-reserves Date: November 21st, 2024 Tags: Crypto, Payments Comments: No

DebtCoin: Reserve Management

This article outlines strategies for managing DebtCoin reserves effectively, focusing on rollout plans, scenario handling, and long-term goals.

Rollout

DebtCoin will launch with an ICO, selling tokens at a discount (e.g., 90% of the debt price) to early adopters. Initial proceeds will cover operations and currency development. Restrictions, like throttled selling, will prevent rapid profit-taking.

At launch, reserves won’t match a 1:1 ratio. The short-term goal will be to achieve parity, the mid-term to exceed it. User investments will be directed to low-risk instruments such as Treasury bills and TIPS, aligning reserve growth with inflation. This will help stabilize DebtCoin’s value and ensure liquidity during sudden liquidations. Transparency through real-time reserve tracking and third-party audits will build trust.

Scenario Handling

Scenario 1: Rapid Debt Increase

- High Liquidations: Holders may sell to lock in profits. To manage, the system could implement phased liquidations (paying a portion immediately and the rest say, over two weeks) and dynamic transaction fees.